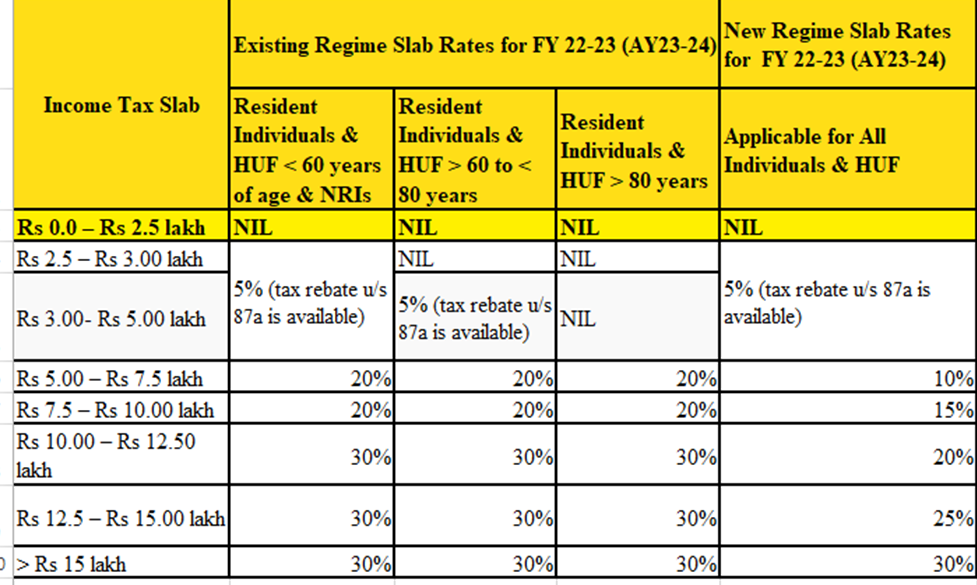

| Income Tax Slab | New Regime Income Tax Slab Rates FY 2021-22 (Applicable for All Individuals & HUF) |

| Rs 0.0 – Rs 2.5 lakh | NIL |

| Rs 2.5 lakh – Rs 3.00 lakh | 5% (tax rebate u/s 87a is available) |

| Rs 3.00 lakh – Rs 5.00 lakh | |

| Rs 5.00 lakh- Rs 7.5 lakh | 10% |

| Rs 7.5 lakh – Rs 10.00 lakh | 15% |

| Rs 10.00 lakhs – Rs 12.50 lakh | 20% |

| Rs 12.5 lakhs – Rs 15.00 lakh | 25% |

| > Rs 15 lakh | 30% |

NOTE:

- Please note that the tax rates in the New tax regime is the same for all categories of Individuals, i.e Individuals & HUF upto 60 years of age, Senior citizens above 60 years upto 80 years , and Super senior citizens above 80 years. Hence no increased basic exemption limit benefit will be available to senior and super senior citizens in the New Tax regime.

- Individuals with Net taxable income less than or equal to Rs 5 lakh will be eligible for tax rebate u/s 87A i.e tax liability will be nil of such individual in both – New and old/existing tax regimes

- Basic exemption limit for NRIs is of Rs 2.5 Lakh irrespective of age.

- Additional Health and Education cess at the rate of 4 % will be added to the income tax liability in all cases. (increased from 3% since FY 18-19)

- Surcharge applicable as per tax rates below in all categories mentioned above:

- 10% of Income tax if total income > Rs.50 lakh

- 15% of Income tax if total income > Rs.1 crore

- 25% of Income tax if total income > Rs.2 crore

- 37% of Income tax if total income > Rs.5 crore

Income tax slabs for individual aged below 60 years & HUF

| Income Tax Slab | Individuals Below The Age Of 60 Years – Income Tax Slabs |

| Up to Rs 2.5 lakh | NIL |

| Rs. 2.5 lakh -Rs. 5 lakh | 5% |

| Rs 5.00 lakh – Rs 10 lakh | 20% |

| > Rs 10.00 lakh | 30% |

- Income tax exemption limit is up to Rs 2,50,000 for Individuals , HUF below 60 years aged and NRIs.

- An additional 4% Health & education cess will be applicable on the tax amount calculated as above.

- Surcharge:

- 10% of income tax, where total income exceeds Rs.50 lakh up to Rs.1 crore.

- 15% of income tax, where the total income exceeds Rs.1 crore.

Conditions for opting New Tax regime.

The taxpayer opting for concessional rates in the New Tax regime will have to forgo certain exemptions and deductions available in the existing old tax regime. In all there are 70 deductions & exemptions that are not allowed, out of which the most commonly used are listed below:

List of common Exemptions and deductions “ not allowed” under New Tax rate regime

- Leave Travel Allowance (LTA)

- House Rent Allowance (HRA)

- Conveyance allowance

- Daily expenses in the course of employment

- Relocation allowance

- Helper allowance

- Children education allowance

- Other special allowances [Section 10(14)]

- Standard deduction on salary

- Professional tax

- Interest on housing loan (Section 24)

- Deduction under Chapter VI-A deduction (80C,80D, 80E and so on) (Except Section 80CCD(2))

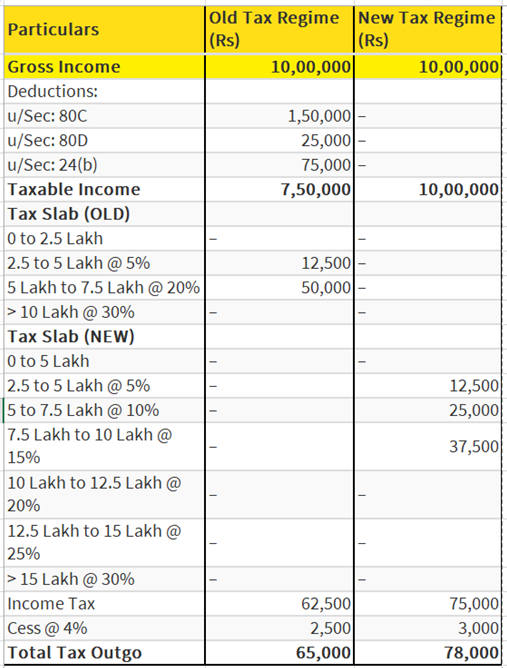

Let’s take an example of comparing the Old & New tax regime of an assessee with Rs 10 Lakh income.

Mr. Vishal Sakpal has a salary income of Rs 10 lakh. His total investment u/s 80C is Rs 1.7 lakh under ELSS, PF, LIC premium and principal installment of home loan. Further he pays Medical insurance for himself and his wife of Rs 28,000. If he opts for the old tax regime, then he can claim the above deductions, however if he wishes to go for a new tax regime than these deductions will not be available. He has paid home loan interest of Rs 75,000 in FY 2022-23. Let us see the tax outflow in both the regimes.